A global study of over 300 banking and financial services executives shows that, for the first time, innovation is ranked as important as regulation.

The research also reveals that mobile first has now become mainstream, while innovative disruptive technologies such as block-chain will potentially become a very attractive alternative to traditional payment methods, transforming payment processing and acting as significant drivers for change this year.

The fourth annual report, ‘The Changing Face of Payments: A Review of Current Payments Infrastructures and Implications for the Future’, predicts that several trends have reached their tipping point. According to 90% of responses, mobile devices will represent a mainstream option for person-to-person or person-to-business payments within the next five years.

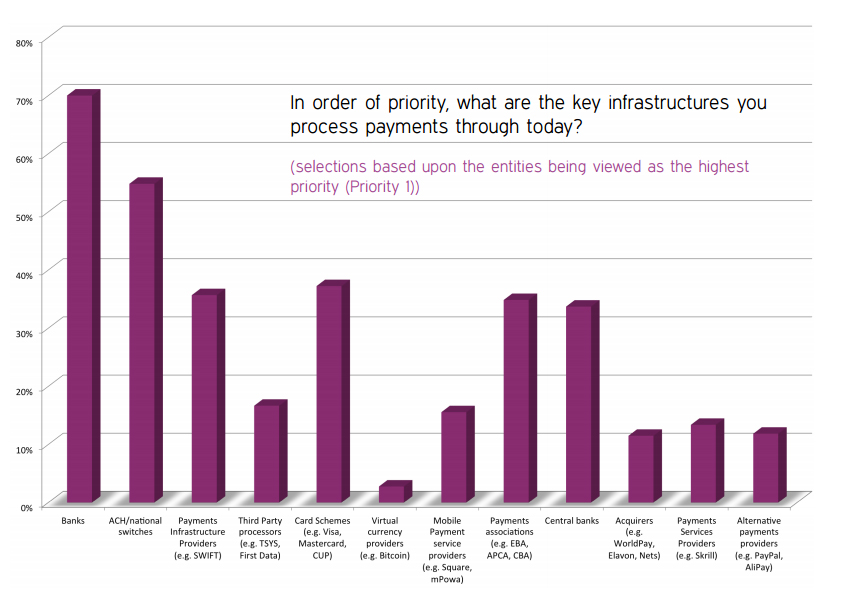

What are the key infrastructures you process payments through today?

Digital wallet features continue to be developed, a trend encapsulated by the launch of Apple Pay, which has made such offerings more accessible. The executives surveyed predict the continued influence of such brands, with 39% of responses suggesting that Apple and Google will dominate mobile payments over the next five years.

The study also highlights that cryptocurrency and block-chain technologies are now seen as real drivers for change and are gaining mainstream recognition, particularly in back-office infrastructures.

The emergence of digital-only lenders such as Atom Bank in the UK emphasises the conversion of previously marginal initiatives into the everyday. However, the report has one caveat: that regulation and the use of cryptocurrency markets and Bitcoin will potentially be a major issue for payments regulators and participants in 2015, not least given how fast these new entrants have evolved from emerging technologies to real contenders in the payments industry.

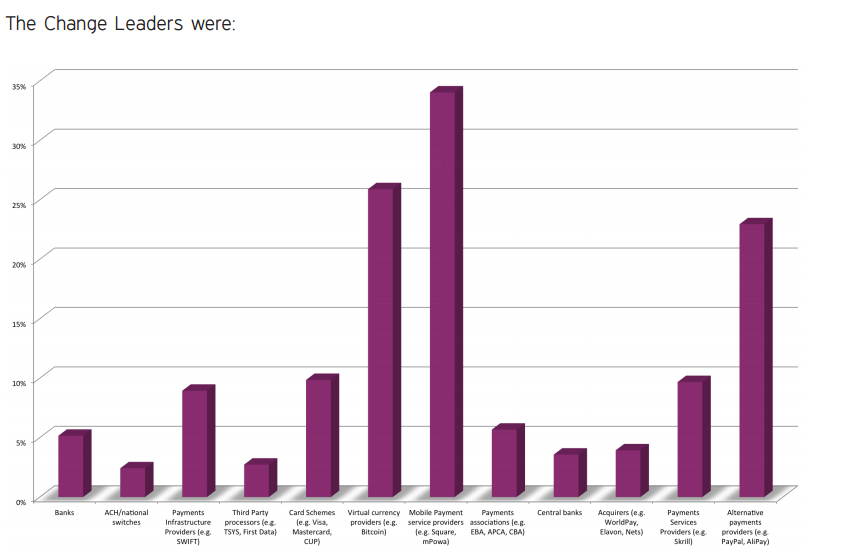

Change leaders in processing infrastructure

For the first time, regulation is not seen as stifling innovation anymore and those surveyed rank the two as equally important in terms of short-term industry development (32% and 33% respectively for banks, and 34% by those from non-banks).

However, innovation is seen as far more important in the long-term, due to competition, market opportunities and an ever-increasing need for more agility for faster time to market solutions (29% of all surveyed consider innovation a priority, compared to 17% for regulation).

Both regulation and innovation are now key considerations for companies striving to optimise customer journeys that are cost efficient, safe, flexible and secure, making them a real investment priority. The importance of innovation is being driven in particular by new entrants to the industry that are major sources of disruption in establishing new ways to pay and to disintermediate or differentiate in a fluid market.

“The payments industry continues to face an unprecedented pace and scale of change, driven by a potent mix of social, technological, political, competitive and regulatory factors,” says Tony Virdi, Vice President of Cognizant’s Banking and Financial Services Practice for the UK and Ireland.

“Innovation is crucial and traditional players need to adapt quickly, with agile and secure technologies to improve their business models and deliver better customer experience. The speed at which these innovative concepts have developed from ‘new kids on the block’ to major agents for change is extraordinary and the key to winning in the ‘Innovation Game’ is to be a part of it. It is essential that financial institutions are able to diagnose, adapt and respond to the changing market with agility in order to respond to ever evolving customer needs – a positive customer experience is key.”